"One of the true tests of leadership is the ability to recognize a problem before it becomes an emergency." - Arnold H Glasgow

We all knew that the Fiscal Cliff was approaching(we have known this for four years) and we all knew that the leadership of the United States would wait until the last minute to try to come to a resolution. It is clear that no resolution will be found between now and the end of the year and if one is found it will be another band aid placed on a fractured skull. There is no way to complete a proper working solution to this monumental problem in three days.

Furthermore while this is being debated the news reels report that they are coming together, falling apart, working bilaterally, working unilaterally, not working at all and any other fodder to make their readers more confused than ever. The noise from the press is creating a sense of urgency when in actual fact the Obama agenda is very clear - let the Fiscal Cliff happen as it was a Bush era tax cut that should be reversed. Drag the economy into recession and point a finger at the other side for creating the mess. Once again more finger pointing and no leadership.

As this all bubbles to the surface the debt ceiling is ounce again looming its head. The Treasury Secretary, Timothy Geithner, has said that the United States will reach the debt ceiling of $16.4 trillion by the end of the year. This level of debt is now over 100 percent of GDP and is accelerating at a rate of around 6 percent a year, more than triple the growth of GDP!

Now he will still be able to pay bills through February by moving money around in a take from Peter to pay Paul scenario but this too needs to be addressed. As the Obama administration will spend more than a trillion a year for the next four years the ceiling will need to be raised but this once again circles round to the Fiscal Cliff and how much in additional taxes will be received once the Bush tax cuts expire. A mess to be sure and one that has been left far too late once again showing that our current leadership (and I am talking about both sides of the isle) has one thing on its mind - saving their jobs!

How much longer can this leadership vacuum last before the people have had enough? Surprisingly the vote for more of the same was overwhelming but in in times of economic weakness it is not that difficult to buy votes by creating unfunded social programs. The problem now is that paying for these programs is becoming harder and harder to do and all the while the debt rises faster and faster. This debt will need to be repaid or at the very least a plan worked out on how to balance the budget, but the political bickering is creating a void between the politicians and reality and this is not an environment where a workable solution will be found. More often than not this is an environment where the economy runs into a brick wall at high speed.

Therefore in this type of political environment it is extremely important to protect your assets. The risks to investing in the stock market far outweigh any perceived upside as there is no way to hazard a vague guess as to the outcome. We are clearly at the mercy of our political leadership and it is very clear that no leader exists so investing in the market is like taking a ride on a sailboat without attending to the rudder.

I would like to take this opportunity to wish all my readers a wonderful New Year and a very prosperous 2013.

Friday, December 28, 2012

Friday, December 21, 2012

The Return of the HELOC

"If one considered life as a simple loan, one would perhaps be less exacting. We possess actually nothing; everything goes through us." - Eugene Delacroix

Back in the heyday of the housing bubble HELOCs (home equity lines of credit) were used as a type of a cash machine by the consumer. For six years over $110 billion dollars a year was withdrawn from the equity of houses. Consumers viewed it as money that was theirs and spent it freely creating a massive surge for consumer goods and services. Banks wanting to make money (as always) piled into the fray and issued HELOCs up to 125 percent of the value of the homeowner's residence. The thought was that the price of housing would never go down so this money was safe.

Well when the bubble in housing burst these HELOCs resulted in homeowners losing their houses as suddenly they owed far more than the house was worth. In addition without the support of a consumer willing to spend money the economy itself contracted and the homeowner was suddenly out of a job. The spiral started as quickly as it had begun and the rest as they say is history.

Six years later banks are still dealing with the mess. To date they have written off more than $4 billion in debt and there is still a long way to go. As an example assume that the total debt on the house is $500,000 and the value of the house is $400,000, on paper the bank has lost $100,000 but it is always worse than that. First you have to reduce the value to the bank by the agent commissions and closing costs and then there may be other liens such as HOA and taxes. All in all the bank would be lucky in this example to net $350,000 a 50% increase in the loss!

Given this backdrop I was surprised to read that 2012 is expected to see a 30 percent rise in HELOCs. The estimate is that just under $80 billion in debt will be offered to homeowners through HELOCs this year. Furthermore it is expected that 2013 will see over $110 billion issued in HELOC debt, more than the average issued during the housing bubble. This will definitely have an impact on consumer liquidity and should result in decent consumer spending growth however I wonder if this rise in HELOC debt is a good thing.

Certainly lenders will have far stricter criteria for issuing a HELOC than before and there is over $7.3 trillion in home equity in the United States so the amount lent in HELOC loans is small. In addition the rates attached to the loans are very attractive so the question remains where will the proceeds be invested?

During the housing bubble consumers spent money on everything from upgrading their house to buying boats and overseas trips. It was one big party funded by the banks. Looking around now there are opportunities to invest into real estate, private equity and a few select stocks however outside of this the investment world is very tentative. In most cases a homeowner's house is their largest asset so it needs to be treated with care.

There is the thought that you can get the HELOC and keep it for emergencies and I am sure that a decent amount of this money will be used for that purpose. Outside of this I am hopeful that the remaining proceeds are being put to good use and invested wisely as if anything was learnt during the housing bubble it was that spending it on a big Holiday Season will not end in Ho Ho Ho but rather with a No No No. From me to you have a very Happy Holiday!

Back in the heyday of the housing bubble HELOCs (home equity lines of credit) were used as a type of a cash machine by the consumer. For six years over $110 billion dollars a year was withdrawn from the equity of houses. Consumers viewed it as money that was theirs and spent it freely creating a massive surge for consumer goods and services. Banks wanting to make money (as always) piled into the fray and issued HELOCs up to 125 percent of the value of the homeowner's residence. The thought was that the price of housing would never go down so this money was safe.

Well when the bubble in housing burst these HELOCs resulted in homeowners losing their houses as suddenly they owed far more than the house was worth. In addition without the support of a consumer willing to spend money the economy itself contracted and the homeowner was suddenly out of a job. The spiral started as quickly as it had begun and the rest as they say is history.

Six years later banks are still dealing with the mess. To date they have written off more than $4 billion in debt and there is still a long way to go. As an example assume that the total debt on the house is $500,000 and the value of the house is $400,000, on paper the bank has lost $100,000 but it is always worse than that. First you have to reduce the value to the bank by the agent commissions and closing costs and then there may be other liens such as HOA and taxes. All in all the bank would be lucky in this example to net $350,000 a 50% increase in the loss!

Given this backdrop I was surprised to read that 2012 is expected to see a 30 percent rise in HELOCs. The estimate is that just under $80 billion in debt will be offered to homeowners through HELOCs this year. Furthermore it is expected that 2013 will see over $110 billion issued in HELOC debt, more than the average issued during the housing bubble. This will definitely have an impact on consumer liquidity and should result in decent consumer spending growth however I wonder if this rise in HELOC debt is a good thing.

Certainly lenders will have far stricter criteria for issuing a HELOC than before and there is over $7.3 trillion in home equity in the United States so the amount lent in HELOC loans is small. In addition the rates attached to the loans are very attractive so the question remains where will the proceeds be invested?

During the housing bubble consumers spent money on everything from upgrading their house to buying boats and overseas trips. It was one big party funded by the banks. Looking around now there are opportunities to invest into real estate, private equity and a few select stocks however outside of this the investment world is very tentative. In most cases a homeowner's house is their largest asset so it needs to be treated with care.

There is the thought that you can get the HELOC and keep it for emergencies and I am sure that a decent amount of this money will be used for that purpose. Outside of this I am hopeful that the remaining proceeds are being put to good use and invested wisely as if anything was learnt during the housing bubble it was that spending it on a big Holiday Season will not end in Ho Ho Ho but rather with a No No No. From me to you have a very Happy Holiday!

Friday, December 14, 2012

China's Debt Problem

"Well, we lost a lot of our independence already. We are dependent on China for credit. We are dependent on Middle Eastern countries for energy supplies. And many Americans are dependent on the government for their income, health care, education of their children, food stamps." - Jim DeMint

It is common knowledge that China has enormous capital reserves. A current estimate is that the government in China is sitting on a foreign exchange reserve of more than $3 trillion. This money has been deployed into United States treasuries, Euro bonds, gold and many other mainstream investments and it is thought that with this stockpile of cash and reserves that they will be able to manage any kind of economic slowdown without much trouble.

That theory is now being questioned due to the fact that their banking system has shown many structural flaws and Europe, which makes up around 40 percent of all Chinese exports, is struggling. Both of these are causing a weakness in the balance of payments but aside from that there is the threat that an economic slowdown in China could destabilize its political structure.

As more and more of the Chinese population becomes mobile there is a desire and a demand for living standards to improve. The only way that this can be achieved is for China to continue to grow at a rate north of 6 percent. This is an extremely fast clip for a nation as large as China but it was achievable during the last decade due to the cheapness of its labor pool and a weak currency. Now with the global economic weakness and a rapid increase in labor rates China is being squeezed and this reserve pool looks like it may not be enough. In addition it is starting to appear that the Chinese currency the renminbi is no longer grossly undervalued and manufacturers around the globe are starting to take notice of this and are repatriating work to their local countries.

In order to shore up growth the government has undertaken numerous infrastructure projects many of which are the equivalent of digging holes and filling them up again. Airports lie vacant, subways have no traffic and bridges lead to nowhere. In order to finance this the government has relied heavily on foreign investment but that is beginning to dry up as many of these projects are turning out to be alligators. During the second quarter China's capital account shrunk by $110 billion as capital fled the country so China is now having to finance these projects itself using its capital reserves.

This is creating another problem as when foreign capital moves into a country it is forced to exchange it for local currency. This flows into the banking system and results in banks being awash with reserve so it starts to offer loans to locals. A reverse of this trend shrinks the capital base and results in a contraction of the loan pool. The issue is that a lot of the loans that were made are turning sour. Companies that took out the loans are closing down as demand for their goods and services is not keeping up with the ever spiralling debt payments.

The bulk of these loans were made back in 2008 and are now coming back to haunt the government as a big portion of these loans were made to state owned businesses many of whom are running deep in the red already. The state will then have to fund these obligations whether it likes it or not and this will have another major drag on its capital base. In the boom years overcapacity at steel plants and such was considered a necessary requirement to fill expected demand but with this demand gone these investments are turning into a black hole.

Currently the total corporate debt level is at roughly 125 percent of total GDP. This is up from 110 percent in 2008. Now the size is not a major problem if the economy can continue to grow at 8 percent and the growth in borrowing slows. However now that the global economy is stuttering and there is no sign that a recovery is imminent China's reserves are looking very weak and this will have major implications around the globe particularly if they have to start to claw back their massive foreign investment pool.

It is common knowledge that China has enormous capital reserves. A current estimate is that the government in China is sitting on a foreign exchange reserve of more than $3 trillion. This money has been deployed into United States treasuries, Euro bonds, gold and many other mainstream investments and it is thought that with this stockpile of cash and reserves that they will be able to manage any kind of economic slowdown without much trouble.

That theory is now being questioned due to the fact that their banking system has shown many structural flaws and Europe, which makes up around 40 percent of all Chinese exports, is struggling. Both of these are causing a weakness in the balance of payments but aside from that there is the threat that an economic slowdown in China could destabilize its political structure.

As more and more of the Chinese population becomes mobile there is a desire and a demand for living standards to improve. The only way that this can be achieved is for China to continue to grow at a rate north of 6 percent. This is an extremely fast clip for a nation as large as China but it was achievable during the last decade due to the cheapness of its labor pool and a weak currency. Now with the global economic weakness and a rapid increase in labor rates China is being squeezed and this reserve pool looks like it may not be enough. In addition it is starting to appear that the Chinese currency the renminbi is no longer grossly undervalued and manufacturers around the globe are starting to take notice of this and are repatriating work to their local countries.

In order to shore up growth the government has undertaken numerous infrastructure projects many of which are the equivalent of digging holes and filling them up again. Airports lie vacant, subways have no traffic and bridges lead to nowhere. In order to finance this the government has relied heavily on foreign investment but that is beginning to dry up as many of these projects are turning out to be alligators. During the second quarter China's capital account shrunk by $110 billion as capital fled the country so China is now having to finance these projects itself using its capital reserves.

This is creating another problem as when foreign capital moves into a country it is forced to exchange it for local currency. This flows into the banking system and results in banks being awash with reserve so it starts to offer loans to locals. A reverse of this trend shrinks the capital base and results in a contraction of the loan pool. The issue is that a lot of the loans that were made are turning sour. Companies that took out the loans are closing down as demand for their goods and services is not keeping up with the ever spiralling debt payments.

The bulk of these loans were made back in 2008 and are now coming back to haunt the government as a big portion of these loans were made to state owned businesses many of whom are running deep in the red already. The state will then have to fund these obligations whether it likes it or not and this will have another major drag on its capital base. In the boom years overcapacity at steel plants and such was considered a necessary requirement to fill expected demand but with this demand gone these investments are turning into a black hole.

Currently the total corporate debt level is at roughly 125 percent of total GDP. This is up from 110 percent in 2008. Now the size is not a major problem if the economy can continue to grow at 8 percent and the growth in borrowing slows. However now that the global economy is stuttering and there is no sign that a recovery is imminent China's reserves are looking very weak and this will have major implications around the globe particularly if they have to start to claw back their massive foreign investment pool.

Friday, December 7, 2012

Jobs Up Sentiment Down

"Living at risk is jumping off a cliff and build the wings on the way down." - Ray Bradbury

Today we received some more positive news on the job front with the number of jobs growing faster than expected. Furthermore the unemployment rate fell to 7.7 percent but this number once again masked the fact that a lot of the improvement to the unemployment number was due to the fact that more and more people are just giving up searching for a job.

Of more interest is the fact that consumer confidence fell sharply in as consumers finally are coming to terms with the massive economic impact of the approaching Fiscal Cliff. Normally consumer confidence rises with good jobs reports but not this time. With the thought of taxes spiralling higher and the probability of the effects dragging economic growth lower the number plunged from 82.7 to 74.5. Combined with this number is the Future Expectation Index which dropped to its lowest reading since December 2011.

So with jobs still hard or impossible to find and with the impact of the Fiscal Cliff approaching consumers are skittish and this does not bode well for both the holiday shopping season and the economy in 2013. As I have mentioned repeatedly, consumers and investors need to wake up and realize that this slow growth scenario is going to be around for a long time and that coupled with this are low rates of return on investments.

Gone are the days of earning 5 or 6 percent real rates of return (a real rate of return is the rate of return in excess of inflation). In its place are rates that are lucky to even be positive. In this environment you need to make sure that your portfolio is protected against any downside shocks as recovery from these will take years if not decades. In place of risk you need to seek out a portfolio that protects your assets and to me this should include gold, properties and alternative investments such as private equity.

With all the risks that abound at present leveraging up in the stock market just does not make sense so protect your assets even if it means remaining in cash for an extended period.

Today we received some more positive news on the job front with the number of jobs growing faster than expected. Furthermore the unemployment rate fell to 7.7 percent but this number once again masked the fact that a lot of the improvement to the unemployment number was due to the fact that more and more people are just giving up searching for a job.

Of more interest is the fact that consumer confidence fell sharply in as consumers finally are coming to terms with the massive economic impact of the approaching Fiscal Cliff. Normally consumer confidence rises with good jobs reports but not this time. With the thought of taxes spiralling higher and the probability of the effects dragging economic growth lower the number plunged from 82.7 to 74.5. Combined with this number is the Future Expectation Index which dropped to its lowest reading since December 2011.

So with jobs still hard or impossible to find and with the impact of the Fiscal Cliff approaching consumers are skittish and this does not bode well for both the holiday shopping season and the economy in 2013. As I have mentioned repeatedly, consumers and investors need to wake up and realize that this slow growth scenario is going to be around for a long time and that coupled with this are low rates of return on investments.

Gone are the days of earning 5 or 6 percent real rates of return (a real rate of return is the rate of return in excess of inflation). In its place are rates that are lucky to even be positive. In this environment you need to make sure that your portfolio is protected against any downside shocks as recovery from these will take years if not decades. In place of risk you need to seek out a portfolio that protects your assets and to me this should include gold, properties and alternative investments such as private equity.

With all the risks that abound at present leveraging up in the stock market just does not make sense so protect your assets even if it means remaining in cash for an extended period.

Friday, November 30, 2012

The United States - A Manufacturing Superpower

"China's history is marked by thousands of years of world-changing innovations: from the compass and gunpowder to acupuncture and the printing press. No one should be surprised that China has re-emerged as an economic superpower." - Gary Locke

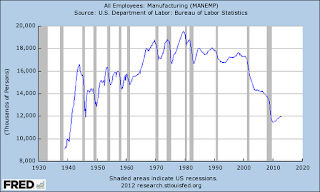

It is common belief that China has taken over as the world's top manufacturing country. It is clear that millions of jobs have left the United States (see the first chart below) and have moved to cheap labor hubs such as China and other countries in the East, however the thought that manufacturing in the United States is dead is a misguided opinion. Could there be a resurgence in United States manufacturing and could this be the key to lowering the unemployment rate?

Having been dogged by a high unemployment rate for the past number of years, getting this number lower is of critical importance to the economic strength of the United States. More jobs mean more income to the populous who in turn have more money to spend and therefore buy more goods and services, reviving a weak economy, creating growth and economic strength. As there have been a glut of jobs moved off shore it is felt that creating tariffs and other barriers is in the best interest of the United States but this is to me a short sighted view and I will argue that because of the lack of barriers the United States has once again become one of the world's manufacturing superpowers.

In watching the trends more and more manufacturers are bringing the work back onto American soil for a number of reasons but first and foremost is the ability to remain price competitive. So how is this possible when labor rates are so much cheaper in the East? Through productivity gains meaning more product is produced per person in the United States offsetting the cost per hour and leveling the playing field. As you can see in the next set of graphs that the gains in productivity have continued unabated for years and this is starting to tilt the economic advantage in favor of the United States.

This productivity has lead to a resurgence of manufacturing in the United States which has virtually surpassed the pre-recession levels. In fact taken on its own the value of manufactured product in the United States would make it the 9th largest economy in the world.

Another benefit is that with the productivity comes the ability to pay the workers an excellent wage for their work particularly in comparison to their offshore brethren.

As Germany has proven, it is possible to keep manufacturing healthy even with an expensive workforce as long as you become extremely efficient and continue to improve productivity and it appears on the surface that the United States has embraced this and has returned to a manufacturing superpower. So why haven't the jobs returned?

Now here is the rub, in order to remain competitive the good old production and manufacturing job has gone. There is no way that America (or the rest of the world for that matter) can compete with the wages of the East. When bodies are needed to produce something they have the comparative advantage however when there is a highly skilled manufacturing process required, the West still holds an advantage particularly when you factor in the costs of shipping the product and the potential threat to an infringement on your patented product (having knock offs of your product magically appear on shelves in the East before the actual product even reaches American soil).

For these reasons numerous manufacturers are returning to the United States and are reaping the rewards of short delivery time and low delivery cost plus the social benefit of stamping Made in America on the product. This work however requires a skilled labor force as the bulk of the basic manufacturing work has been replaced with technology in the form of robots and other efficiencies. The good old days of being good with ones hands and therefore finding a job are for all intents and purposes gone from the United States and many other first world economies.

So looking forward while it appears that manufacturing is on the upswing the demand for workers will not come from this part of the economy. Workers will have to attend career colleges (we used to call them trade schools) in order to retool their skills and get back into manufacturing as these jobs now require a heavy dose of mathematics, science and technological know how to become employed. The good news is that these workers should earn a wonderful income for years to come but manufacturing as an employment driver is dead. I believe that this is why there is such an outcry over the loss of unskilled job opportunities. Over time the system will adjust and we will all benefit from the advancement in manufacturing but until then, there will be an extended drag of high unemployment in the United States for far longer than anyone ever anticipated and this drag will be felt throughout the economy for years to come.

It is common belief that China has taken over as the world's top manufacturing country. It is clear that millions of jobs have left the United States (see the first chart below) and have moved to cheap labor hubs such as China and other countries in the East, however the thought that manufacturing in the United States is dead is a misguided opinion. Could there be a resurgence in United States manufacturing and could this be the key to lowering the unemployment rate?

Having been dogged by a high unemployment rate for the past number of years, getting this number lower is of critical importance to the economic strength of the United States. More jobs mean more income to the populous who in turn have more money to spend and therefore buy more goods and services, reviving a weak economy, creating growth and economic strength. As there have been a glut of jobs moved off shore it is felt that creating tariffs and other barriers is in the best interest of the United States but this is to me a short sighted view and I will argue that because of the lack of barriers the United States has once again become one of the world's manufacturing superpowers.

In watching the trends more and more manufacturers are bringing the work back onto American soil for a number of reasons but first and foremost is the ability to remain price competitive. So how is this possible when labor rates are so much cheaper in the East? Through productivity gains meaning more product is produced per person in the United States offsetting the cost per hour and leveling the playing field. As you can see in the next set of graphs that the gains in productivity have continued unabated for years and this is starting to tilt the economic advantage in favor of the United States.

This productivity has lead to a resurgence of manufacturing in the United States which has virtually surpassed the pre-recession levels. In fact taken on its own the value of manufactured product in the United States would make it the 9th largest economy in the world.

Another benefit is that with the productivity comes the ability to pay the workers an excellent wage for their work particularly in comparison to their offshore brethren.

As Germany has proven, it is possible to keep manufacturing healthy even with an expensive workforce as long as you become extremely efficient and continue to improve productivity and it appears on the surface that the United States has embraced this and has returned to a manufacturing superpower. So why haven't the jobs returned?

Now here is the rub, in order to remain competitive the good old production and manufacturing job has gone. There is no way that America (or the rest of the world for that matter) can compete with the wages of the East. When bodies are needed to produce something they have the comparative advantage however when there is a highly skilled manufacturing process required, the West still holds an advantage particularly when you factor in the costs of shipping the product and the potential threat to an infringement on your patented product (having knock offs of your product magically appear on shelves in the East before the actual product even reaches American soil).

For these reasons numerous manufacturers are returning to the United States and are reaping the rewards of short delivery time and low delivery cost plus the social benefit of stamping Made in America on the product. This work however requires a skilled labor force as the bulk of the basic manufacturing work has been replaced with technology in the form of robots and other efficiencies. The good old days of being good with ones hands and therefore finding a job are for all intents and purposes gone from the United States and many other first world economies.

So looking forward while it appears that manufacturing is on the upswing the demand for workers will not come from this part of the economy. Workers will have to attend career colleges (we used to call them trade schools) in order to retool their skills and get back into manufacturing as these jobs now require a heavy dose of mathematics, science and technological know how to become employed. The good news is that these workers should earn a wonderful income for years to come but manufacturing as an employment driver is dead. I believe that this is why there is such an outcry over the loss of unskilled job opportunities. Over time the system will adjust and we will all benefit from the advancement in manufacturing but until then, there will be an extended drag of high unemployment in the United States for far longer than anyone ever anticipated and this drag will be felt throughout the economy for years to come.

Friday, November 23, 2012

The Biggest Risk to Your Portfolio

"Only those who will risk going too far can possibly find out how far one can go." - T.S. Eliot

What a great quote from Mr. Eliot. So often in life we give up too soon and it is those that keep trying and pushing that make it in the end. I remember reading a book about John Paul Getty the oil tycoon who said that there were plenty of times in his early years when he had run out of money but he willed his team to drill just a couple more feet and suddenly oil was struck. So do we need to risk it all to make the gains needed and is this risk really necessary?

Well the first thing to consider is the greatest risk to your portfolio which is that it is exhausted before you die. In talking to my life insurance agent the other day she told me that it is now customary to run a life insurance table to 120 years of age, up from 100 just a few years ago. The startling thing to me is that with all the advances in medicine life expectancies are rising dramatically and this will have a profound impact on your retirement. If you are now expected to live more than a decade longer than you planned how would this affect your portfolio and your outlook on retirement?

Well in a simple example let's assume that you retired on $1 million (this would already place you in the top 1% of the globe) and you planned that this would last you 20 years from say 65 to 85. Based on this and a conservative rate of return on your portfolio of 5% (you would not want to risk a dramatic loss on the portfolio at this stage in your life) you would be able to draw roughly $6,000 a month. Now if you live in southern California that is not a lot of money so you move to the Florida or Nevada. Now remember that this amount is set and inflation over the 20 years will erode this amount to a present day value of $3,500 a month (assuming inflation remains contained at 3%), however medical expenses are growing at roughly 20% a year and that is what is needed most as you get old so you are hardly well off. But now let's say that you don't die at 85 but you live to 95, rather than celebrating your longevity you will be pining over the excessive drain on your portfolio.

Well let's assume that you planned better and expected to live the extra 10 years by tacking another 10 years onto the already strained portfolio means that you will now only be able to draw $5,000 a month. The problem is that the spending power will drop much further due to the addition of the extra decade. So by the time you get to 95 the value of your money will have fallen to $2,000 in today's dollars. I think that Florida will be too expensive at this stage which is why a lot of retirees are moving to Mexico, Panama and the like. Not a happy equation but not a problem if you plan correctly.

First off you will more than likely need to work far longer than you expected. Based on the above equation one way to change the numbers around would be to work (assuming you are capable) to 75. In this same vain earning more money would be an obvious solution but one that is not always available however you might want to consider a part time job or moonlighting some of your skills on the side can boost the size of the portfolio considerably. This can also be effective at bringin in some income once you retire. This way your portfolio will have grow and you will be drawing on it for a shorter period. Assuming that it now has grown to $1.5 million you should be fine on $8,000 a month.

The second thing to consider is taking on assisted care insurance. If you are not insured for this I hope that you have a large net worth as a decent care program can cost north of $3,000 a month. The other age old thought is to have a lot of kids and pass the buck over to them, but to me that is a last resort but unfortunately one that forms the backbone of a lot of people's plans.

Third is to cut expenditure and live below your means. I don't know how many times I hear people earning excellent paychecks but they proceed to spend as much or in a lot of cases more than they earn. This is really shooting yourself in the foot. There is no need to keep up with the Jones' particularly if they are living beyond their means. Now if you are earning a lot of money and can adequately afford to upgrade then by all means go ahead but borrowing money for the overseas trip or buying another flashy car just to impress the neighbors should be eliminated in order to ensure that you live a wonderfully balanced and eventful retirement.

Finally is to try to squeeze every last percent out of your investments. You do not have to risk everything to make the investment grow but a one, two or three percent increase in your returns will go a long way to getting you to retirement. Think about this, if I add 1% to the returns in the example above you can draw $7,000 a month up from $6,000 a month. This is over 16% more that you can spend. Now if you can live on say $5,000 a month you will not be drawing on your principle at all. Take this a step further, if you earn 3% extra your investment portfolio will now grow and provide you with more than enough no matter how long you live.

So how do you increase your returns without taking on excessive risk? Obviously taking on risk should be a last resort as investing in a basket of risky assets can leave you high and dry when they do not work out as planned and you can ill afford the effects of that when you are aged 85. No I am talking abut taking a fine tooth comb through your entire portfolio from the cash under the mattress to the investment in a privately held business to see if there are some minor tweaks that you can do to gain that extra percent. This is why Fixed Rate Deposits is such a powerful tool for you as you can earn an extra 3% (or more) over CDs and this will immediately assist you in reaching your goals. And remember that retirement means a lot of things to a lot of people, to me I plan only to retire when that nest egg is so large that I can upgrade my lifestyle and believe me, with all of my plans, it is going to have to be huge.

The main point to the blog is to ensure that you are taking control of your own destiny by fixing the little things which are well within your control as these will make a difference in the years to come. Do not get stuck on an age to retire as that could well be your undoing right from the get go. Rather enjoy what you do so that effectively you are retired while you work! As my golf coach used to say; "The only things you can control are the grip and the stance so make sure you get those two pieces down otherwise you have no chance at all."

What a great quote from Mr. Eliot. So often in life we give up too soon and it is those that keep trying and pushing that make it in the end. I remember reading a book about John Paul Getty the oil tycoon who said that there were plenty of times in his early years when he had run out of money but he willed his team to drill just a couple more feet and suddenly oil was struck. So do we need to risk it all to make the gains needed and is this risk really necessary?

Well the first thing to consider is the greatest risk to your portfolio which is that it is exhausted before you die. In talking to my life insurance agent the other day she told me that it is now customary to run a life insurance table to 120 years of age, up from 100 just a few years ago. The startling thing to me is that with all the advances in medicine life expectancies are rising dramatically and this will have a profound impact on your retirement. If you are now expected to live more than a decade longer than you planned how would this affect your portfolio and your outlook on retirement?

Well in a simple example let's assume that you retired on $1 million (this would already place you in the top 1% of the globe) and you planned that this would last you 20 years from say 65 to 85. Based on this and a conservative rate of return on your portfolio of 5% (you would not want to risk a dramatic loss on the portfolio at this stage in your life) you would be able to draw roughly $6,000 a month. Now if you live in southern California that is not a lot of money so you move to the Florida or Nevada. Now remember that this amount is set and inflation over the 20 years will erode this amount to a present day value of $3,500 a month (assuming inflation remains contained at 3%), however medical expenses are growing at roughly 20% a year and that is what is needed most as you get old so you are hardly well off. But now let's say that you don't die at 85 but you live to 95, rather than celebrating your longevity you will be pining over the excessive drain on your portfolio.

Well let's assume that you planned better and expected to live the extra 10 years by tacking another 10 years onto the already strained portfolio means that you will now only be able to draw $5,000 a month. The problem is that the spending power will drop much further due to the addition of the extra decade. So by the time you get to 95 the value of your money will have fallen to $2,000 in today's dollars. I think that Florida will be too expensive at this stage which is why a lot of retirees are moving to Mexico, Panama and the like. Not a happy equation but not a problem if you plan correctly.

First off you will more than likely need to work far longer than you expected. Based on the above equation one way to change the numbers around would be to work (assuming you are capable) to 75. In this same vain earning more money would be an obvious solution but one that is not always available however you might want to consider a part time job or moonlighting some of your skills on the side can boost the size of the portfolio considerably. This can also be effective at bringin in some income once you retire. This way your portfolio will have grow and you will be drawing on it for a shorter period. Assuming that it now has grown to $1.5 million you should be fine on $8,000 a month.

The second thing to consider is taking on assisted care insurance. If you are not insured for this I hope that you have a large net worth as a decent care program can cost north of $3,000 a month. The other age old thought is to have a lot of kids and pass the buck over to them, but to me that is a last resort but unfortunately one that forms the backbone of a lot of people's plans.

Third is to cut expenditure and live below your means. I don't know how many times I hear people earning excellent paychecks but they proceed to spend as much or in a lot of cases more than they earn. This is really shooting yourself in the foot. There is no need to keep up with the Jones' particularly if they are living beyond their means. Now if you are earning a lot of money and can adequately afford to upgrade then by all means go ahead but borrowing money for the overseas trip or buying another flashy car just to impress the neighbors should be eliminated in order to ensure that you live a wonderfully balanced and eventful retirement.

Finally is to try to squeeze every last percent out of your investments. You do not have to risk everything to make the investment grow but a one, two or three percent increase in your returns will go a long way to getting you to retirement. Think about this, if I add 1% to the returns in the example above you can draw $7,000 a month up from $6,000 a month. This is over 16% more that you can spend. Now if you can live on say $5,000 a month you will not be drawing on your principle at all. Take this a step further, if you earn 3% extra your investment portfolio will now grow and provide you with more than enough no matter how long you live.

So how do you increase your returns without taking on excessive risk? Obviously taking on risk should be a last resort as investing in a basket of risky assets can leave you high and dry when they do not work out as planned and you can ill afford the effects of that when you are aged 85. No I am talking abut taking a fine tooth comb through your entire portfolio from the cash under the mattress to the investment in a privately held business to see if there are some minor tweaks that you can do to gain that extra percent. This is why Fixed Rate Deposits is such a powerful tool for you as you can earn an extra 3% (or more) over CDs and this will immediately assist you in reaching your goals. And remember that retirement means a lot of things to a lot of people, to me I plan only to retire when that nest egg is so large that I can upgrade my lifestyle and believe me, with all of my plans, it is going to have to be huge.

The main point to the blog is to ensure that you are taking control of your own destiny by fixing the little things which are well within your control as these will make a difference in the years to come. Do not get stuck on an age to retire as that could well be your undoing right from the get go. Rather enjoy what you do so that effectively you are retired while you work! As my golf coach used to say; "The only things you can control are the grip and the stance so make sure you get those two pieces down otherwise you have no chance at all."

Friday, November 16, 2012

Places to Find Thanksgiving Cheer

"Let's not be turkeys." - Nassim Taleb

Having stayed up most of the night last night smoking a turkey for my son's class I am already in the thanksgiving spirit. So with Thanksgiving next week I thought that I would look at things that might take the edge off the gloom that is currently weighing on the market. With the aftermath of hurricane Sandy and Apple shareholders being beaten down by over $200 billion in the past few weeks (even with the holiday season expected to boost revenues) it certainly is not easy to find much to be thankful for however I believe that if we look carefully there are places to invest that will put that smile back on the dial and allow you to enjoy that festive spirit.

So how are we to be thankful this thanksgiving? First off we are not turkeys! Nassim Taleb is a crisis manager who bets on the only sure thing that will happen in the market - a crash. Now most of the time he losses money but when the crash happens (and it always does) he wins big. His philosophy is summed up by the quote above. If you think about the turkey he lives 1,094 days in peace and tranquility with his friends on the farm not knowing that day 1,095 everyone will be slaughtered. This is the black swan event that he refers to in his book of the same name. Now we may live longer than the turkey but most of the time we invest like them, we bet that life will provide us with continued moderate returns on our investments forever. While I am no Taleb I do believe in his theories as there is no disputing the evidence which is why I spend a lot of time in this blog trying to educate and protect your investments.

Looking at the market though there are a few areas where I feel there is a buying opportunity. You cannot fight innovation. This is what took Apple from virtual bankruptcy to the world's most prized company in a decade. So what other innovative ideas are out there? One of my favorites is 3D Systems Corp which makes 3 dimensional printers for the home and office. To me this is the way of the future. Imagine that for the holidays instead of buying a new iPhone you bought a printer that could print toys? This is a reality and the stock has appreciated like a rocket.

Another place is the new technology around charging batteries. The technology is already here but only 10 million have been sold so far. The technology I refer to is wireless charging systems. Soon to come to your nearest Starbucks is an insert into the table at which you sit that will automatically recharge your battery on your cell phone and laptop using magnetic fields. Amazing stuff and not only should it boost revenues at Starbucks (no I am not suggesting you buy this stock) it will go a long way to assisting with battery cars. Think about it, you can park your Volt at work and while you sit working it automatically recharges itself by linking to the magnetic field in the garage where you parked. Now that would help offset the $20 a day it costs to park plus it will eliminate the stress of worrying if you will make it home on the remaining charge in your car.

Outside of innovation a relatively safe bet which I have mentioned repeatedly is gold. Now I would not load up exclusively on gold and gold stocks but I believe that it should have a position in your portfolio as if and when that bad day does show up it will serve you well.

Next is housing. This investment should provide safety and some decent returns in the next few years as interest rates are expected to remain low at least until Bernanke's tenor is over (January 2014). Furthermore as the banks are coming to grips with the problem the inventory of nonperforming houses should start to slow which will allow further appreciation. As I mentioned in my last blog I would not buy heavily into the builders but looking at the carnage in the dividend paying REITs and closed end funds could be another alternative.

The fiscal cliff that everyone is talking about has caused carnage to these high dividend payers. The assumption (and I believe it is virtual certainty) is that the tax rate on dividends will be allowed to increase at the end of the year. Due to this tax increase investors have dumped closed end funds and REITs in large quantities more than offsetting the tax increase through the stock value depreciation. Some of these investments are yielding more than 10% after the sell-off and I believe that this could be a good investment for the future as regardless of the tax consequences investors want yield. Locking in the current prices locks in the current yields and as investors settle down you should also get a decent upside kick.

As mentioned before I also believe in generic drug manufacturers and anyone that stands to benefit from Obama care. Outside of these areas I would caution you to remain skeptical of the market in general as the problems Europe faces and the slowdown in China are hurting big business. Furthermore unemployment, while improving is still far too high and the government needs to reign in spending. Now don't let me get started on all the negatives as this is the Thanksgiving blog and the point is that while it may be tough out there with some work and some expert assistance there is always a reason to enjoy thanksgiving.

Having stayed up most of the night last night smoking a turkey for my son's class I am already in the thanksgiving spirit. So with Thanksgiving next week I thought that I would look at things that might take the edge off the gloom that is currently weighing on the market. With the aftermath of hurricane Sandy and Apple shareholders being beaten down by over $200 billion in the past few weeks (even with the holiday season expected to boost revenues) it certainly is not easy to find much to be thankful for however I believe that if we look carefully there are places to invest that will put that smile back on the dial and allow you to enjoy that festive spirit.

So how are we to be thankful this thanksgiving? First off we are not turkeys! Nassim Taleb is a crisis manager who bets on the only sure thing that will happen in the market - a crash. Now most of the time he losses money but when the crash happens (and it always does) he wins big. His philosophy is summed up by the quote above. If you think about the turkey he lives 1,094 days in peace and tranquility with his friends on the farm not knowing that day 1,095 everyone will be slaughtered. This is the black swan event that he refers to in his book of the same name. Now we may live longer than the turkey but most of the time we invest like them, we bet that life will provide us with continued moderate returns on our investments forever. While I am no Taleb I do believe in his theories as there is no disputing the evidence which is why I spend a lot of time in this blog trying to educate and protect your investments.

Looking at the market though there are a few areas where I feel there is a buying opportunity. You cannot fight innovation. This is what took Apple from virtual bankruptcy to the world's most prized company in a decade. So what other innovative ideas are out there? One of my favorites is 3D Systems Corp which makes 3 dimensional printers for the home and office. To me this is the way of the future. Imagine that for the holidays instead of buying a new iPhone you bought a printer that could print toys? This is a reality and the stock has appreciated like a rocket.

Another place is the new technology around charging batteries. The technology is already here but only 10 million have been sold so far. The technology I refer to is wireless charging systems. Soon to come to your nearest Starbucks is an insert into the table at which you sit that will automatically recharge your battery on your cell phone and laptop using magnetic fields. Amazing stuff and not only should it boost revenues at Starbucks (no I am not suggesting you buy this stock) it will go a long way to assisting with battery cars. Think about it, you can park your Volt at work and while you sit working it automatically recharges itself by linking to the magnetic field in the garage where you parked. Now that would help offset the $20 a day it costs to park plus it will eliminate the stress of worrying if you will make it home on the remaining charge in your car.

Outside of innovation a relatively safe bet which I have mentioned repeatedly is gold. Now I would not load up exclusively on gold and gold stocks but I believe that it should have a position in your portfolio as if and when that bad day does show up it will serve you well.

Next is housing. This investment should provide safety and some decent returns in the next few years as interest rates are expected to remain low at least until Bernanke's tenor is over (January 2014). Furthermore as the banks are coming to grips with the problem the inventory of nonperforming houses should start to slow which will allow further appreciation. As I mentioned in my last blog I would not buy heavily into the builders but looking at the carnage in the dividend paying REITs and closed end funds could be another alternative.

The fiscal cliff that everyone is talking about has caused carnage to these high dividend payers. The assumption (and I believe it is virtual certainty) is that the tax rate on dividends will be allowed to increase at the end of the year. Due to this tax increase investors have dumped closed end funds and REITs in large quantities more than offsetting the tax increase through the stock value depreciation. Some of these investments are yielding more than 10% after the sell-off and I believe that this could be a good investment for the future as regardless of the tax consequences investors want yield. Locking in the current prices locks in the current yields and as investors settle down you should also get a decent upside kick.

As mentioned before I also believe in generic drug manufacturers and anyone that stands to benefit from Obama care. Outside of these areas I would caution you to remain skeptical of the market in general as the problems Europe faces and the slowdown in China are hurting big business. Furthermore unemployment, while improving is still far too high and the government needs to reign in spending. Now don't let me get started on all the negatives as this is the Thanksgiving blog and the point is that while it may be tough out there with some work and some expert assistance there is always a reason to enjoy thanksgiving.

Friday, November 9, 2012

The Obama Investment

"We're living under the Obama economy. Any CEO in America with a record like this after three years on the job would be graciously shown the door." - Mitch McConnell

Obama is back and I must admit that to many a business owner this is not the outcome that was desired. Interestingly though the rest of the world is relieved and believes that he is the man for the job. That said there is little anyone can do about it now but plan and prepare our investments to benefit during the next four years under his administration. Having already had four years with him to date it is not a really big stretch to expect much of the same, so how can you position yourself to take advantage of his policies?

Well regardless of this week's movement in the stock market this is one of the best performing asset classes during the last four years. The question is can this continue? As long time followers of my blog know I am very skeptical about that but I do believe as you will see below that there are pockets of investments that should benefit.

First off, health care reform is as good as implemented. It may get a few tweaks along the way but essentially millions of Americans will be provided with health care regardless of their ability to pay. This should result in a massive boom for the generic drug manufacturers (for full disclosure, this is my largest investment at present). The reason that generic drug manufacturers will get a boost is that the millions of people accessing health benefits will not be able to afford the brand name.

Looking deeper into this space I would stay away from health care providers for the moment as I am still not fully clear how the influx of new, under insured patients will impact their bottom line. Also insurers will have to come to grips with the mandate and I expect that this will also impact their bottom line until everything is ironed out so for now I would avoid investing too heavily in them.

Next is the low interest rate environment. This policy will remain intact. As such I expect treasuries to yield even less in a year than they do today. He is desperate to create a legacy and he does not want to be the President that did not "fix" unemployment. Furthermore with all of the entitlement programs that he has put in place from health care reform to unemployment benefits, continued printing and monetizing of this spending spree will be required. So for now I expect the Federal Reserve to continue to monetize the deficit in such a way as to ensure that interest rates are kept low for the foreseeable future. (As you know I do have a solution to this with my Fixed Rate Deposits program - just saying).

Low interest rates should be good for housing so I would expect REITs and the builders to continue to benefit from this but to be honest I am not a fan of the builders as they still have to sell their inventory into the market. What I do believe in is investment into income producing real estate, whether it is a single family residence or a block of apartments. At present I have invested in both single family residences, mini storage and am looking at trailer parks, all of which are being bolstered by the low interest environment. Not only are these producing a good cash flow but they are also appreciating once again.

Another area to look is precious metals. While these do get a bad rap, they are a place to invest to protect your undercarriage. While I would not be too aggressive here I would allocate roughly 10% of the portfolio into precious metals which should continue to perform well due to the continued global economic problems and the constant and continued monetization of all government debts around the world.

Now there are a number of ways in which to invest into gold. You can buy the physical commodity, invest into coins, buy gold ETFs, take a gamble on futures or invest into the stocks of gold mining companies. Out of all of these I prefer the ETF and the stock trade (although I do trade the futures for added bandwidth). GDX and GDXJ are my two favorites as the value of the gold mining stocks continues to trail the underlying spot price of gold. Once this narrows you will get an upside move in addition to the movement of the spot gold price.

The final place to look as I mentioned in previous blogs is at alternative investments such as private equity. There are a number of opportunities being presented to the astute investor. This opportunity comes from the void left by the banks and should continue for a decent amount of time given Obama's concentration on creating a far more socialist state at the expense of innovation and growth.

So using a very broad brush that is my take on the future and while it may not be the future that a lot of us wanted we have to adapt to the playing field that presented. Riding through all of this is that the good old days of letting your portfolio lie are gone for now. All of the above takes a lot of work so ensure that you are either actively managing the portfolio yourself or find a portfolio manager that will take a vested interest in your well being.

Obama is back and I must admit that to many a business owner this is not the outcome that was desired. Interestingly though the rest of the world is relieved and believes that he is the man for the job. That said there is little anyone can do about it now but plan and prepare our investments to benefit during the next four years under his administration. Having already had four years with him to date it is not a really big stretch to expect much of the same, so how can you position yourself to take advantage of his policies?

Well regardless of this week's movement in the stock market this is one of the best performing asset classes during the last four years. The question is can this continue? As long time followers of my blog know I am very skeptical about that but I do believe as you will see below that there are pockets of investments that should benefit.

First off, health care reform is as good as implemented. It may get a few tweaks along the way but essentially millions of Americans will be provided with health care regardless of their ability to pay. This should result in a massive boom for the generic drug manufacturers (for full disclosure, this is my largest investment at present). The reason that generic drug manufacturers will get a boost is that the millions of people accessing health benefits will not be able to afford the brand name.

Looking deeper into this space I would stay away from health care providers for the moment as I am still not fully clear how the influx of new, under insured patients will impact their bottom line. Also insurers will have to come to grips with the mandate and I expect that this will also impact their bottom line until everything is ironed out so for now I would avoid investing too heavily in them.

Next is the low interest rate environment. This policy will remain intact. As such I expect treasuries to yield even less in a year than they do today. He is desperate to create a legacy and he does not want to be the President that did not "fix" unemployment. Furthermore with all of the entitlement programs that he has put in place from health care reform to unemployment benefits, continued printing and monetizing of this spending spree will be required. So for now I expect the Federal Reserve to continue to monetize the deficit in such a way as to ensure that interest rates are kept low for the foreseeable future. (As you know I do have a solution to this with my Fixed Rate Deposits program - just saying).

Low interest rates should be good for housing so I would expect REITs and the builders to continue to benefit from this but to be honest I am not a fan of the builders as they still have to sell their inventory into the market. What I do believe in is investment into income producing real estate, whether it is a single family residence or a block of apartments. At present I have invested in both single family residences, mini storage and am looking at trailer parks, all of which are being bolstered by the low interest environment. Not only are these producing a good cash flow but they are also appreciating once again.

Another area to look is precious metals. While these do get a bad rap, they are a place to invest to protect your undercarriage. While I would not be too aggressive here I would allocate roughly 10% of the portfolio into precious metals which should continue to perform well due to the continued global economic problems and the constant and continued monetization of all government debts around the world.

Now there are a number of ways in which to invest into gold. You can buy the physical commodity, invest into coins, buy gold ETFs, take a gamble on futures or invest into the stocks of gold mining companies. Out of all of these I prefer the ETF and the stock trade (although I do trade the futures for added bandwidth). GDX and GDXJ are my two favorites as the value of the gold mining stocks continues to trail the underlying spot price of gold. Once this narrows you will get an upside move in addition to the movement of the spot gold price.

The final place to look as I mentioned in previous blogs is at alternative investments such as private equity. There are a number of opportunities being presented to the astute investor. This opportunity comes from the void left by the banks and should continue for a decent amount of time given Obama's concentration on creating a far more socialist state at the expense of innovation and growth.

So using a very broad brush that is my take on the future and while it may not be the future that a lot of us wanted we have to adapt to the playing field that presented. Riding through all of this is that the good old days of letting your portfolio lie are gone for now. All of the above takes a lot of work so ensure that you are either actively managing the portfolio yourself or find a portfolio manager that will take a vested interest in your well being.

Friday, November 2, 2012

A Recovery In The Making?

"The lesson of history is that you do not get a sustained economic recovery as long as the financial system is in crisis." - Ben Bernanke

The news regarding the United States economic recovery was relatively good this week. Barring the business interruption of Sandy which will have an impact on fourth quarter GDP it appears that housing is rapidly finding a base and that banks are finally getting to grips with the problem and are becoming more proactive in writing down debt so that they can clear out the bad wood and start to lend. The question is can the recovery take proper hold and for this to happen jobs need to be created and interest rates need to remain low for a long period of time.

Let's look at job creation first. In recent weeks there has been a slew of companies laying off thousands of workers. Bank of America is laying off 30,000, HP 29,000, Staples, FedEx and others bring the total to over 100,000 jobs. This is not good news and comes in the face of very poor results from some of Wall Street's bell weather stocks. Apple shares have been crushed from a peak of just over $700 to $590 today. Google shares are down over $100. Banking shares continue to languish and the S&P 500 is down 5% over the last two months. This economy needs jobs to maintain its recovery. Wall Street knows it and this is why the markets are turning over. So how do we get that going?

Well ask either of the presidential candidates and they are going to create millions of jobs overnight. We all know that is not going to happen, but I did stumble across one very interesting idea that may have a very good result. What if, instead of paying people unemployment benefits for 99 months we poured that money into removal of the minimum wage? A radical idea to say the least but let me clarify. If there was no minimum wage I know a number of businesses that would hire workers right away. Sure they would only pay them $5 an hour but that is far better than sitting at home wasting away. Once you are back at work the juices start to flow and suddenly you are able to find better opportunities.

Now here is the best part. The government would subsidize the difference between minimum wages and what the company pays the employee. So for example if the worker is paid $5 an hour but the minimum wage is $8 then the government would top up the workers pay at the end of each month. This three dollar difference would be far less costly and far more efficient in getting people back to work than our current program. Once a target of full employment is reached, there would be a slow re-introduction of the minimum wage, there would be a slow transfer of the burden back to the companies reducing the government's involvement. The idea is that at that time the economy would be at full employment so the demand for workers would bring the hourly rate up anyway and this would have the result of slowly reducing the government's burden as things improve. Furthermore a lot of the burden would be offset by the receipt of more tax revenues.

To me this idea has a lot of merit and is far superior to the money printing philosophy that we have in place right now. This philosophy has resulted in an economy that is still stagnant. Furthermore as I have repeatedly mentioned in this blog that the old ideas of pumping money blindly into a black hole are not targeted and are not producing the results that are needed but are creating a fiscal problem of the magnitude never before known.

The second piece of the puzzle is keeping interest rates low. This is key to the continued recovery in housing. A spike in interest rates would cripple the housing recovery which in turn would derail any form of moderate economic recovery. For now it seems that the continued transfer of toxic debt from banks to the Federal Reserve is containing interest rates but rates need to remain low for an extended time without printing money.

The first thing to do is to ensure as best as possible that banks are not involved in risky investments. In an article in Bloomberg it was mentioned that Dodd-Frank has done nothing to curtail banks enthusiasm for taking on risk. Furthermore as we have seen in crisis after crisis not only do bankers not fully understand risk but their greed gets the better of them and they need to be reigned in to abide by strict parameters. Let the hedge funds and alternative investment fund managers handle the risky stuff, banks need to be the backbone of the economy and the only way to do this is to limit the risk by increasing their reserve requirements. This is very simple to do but at present very risky as banks are already struggling to maintain current requirements while they unload their toxic debt. Increasing this now would cripple banks and put a big stake into the heart of their ability to lend. That said it should be ratcheted up over time to ensure that banks are not as vulnerable to systemic shocks as they were.

By strengthening the banking system with increased reserves and by increasing the base of employed workers I would argue that the economy would strengthen attracting foreign investors. This would keep interest rates low for an extended period. The only reason that interest rates would rise in this scenario is if magically Europe fixed its problems and there was reduced demand for perceived risk free investments. At this point interest rates would have to rise to attract investment. Outside of that unless inflation spikes interest rates should remain low, maybe not at the low levels they are right now but certainly not at massively elevated levels that people fear. A strong US economy would produce the desired result particularly while Europe struggles.

All of these ideas are relatively simple to implement but like any idea it would take time to produce the expected results however I believe those results would be achieved far quicker and far more cheaply than our current strategy. In the meantime we will have to deal with the approaching fiscal cliff and a globe that continues to be mired in uncertainty. Worse still we have an economy that does not have a repaired financial system and an economy that appears to be on the verge of a recession. Weak earnings, recession in Europe and problems in the United States are no reason to stay invested in an over inflated stock market.

The news regarding the United States economic recovery was relatively good this week. Barring the business interruption of Sandy which will have an impact on fourth quarter GDP it appears that housing is rapidly finding a base and that banks are finally getting to grips with the problem and are becoming more proactive in writing down debt so that they can clear out the bad wood and start to lend. The question is can the recovery take proper hold and for this to happen jobs need to be created and interest rates need to remain low for a long period of time.

Let's look at job creation first. In recent weeks there has been a slew of companies laying off thousands of workers. Bank of America is laying off 30,000, HP 29,000, Staples, FedEx and others bring the total to over 100,000 jobs. This is not good news and comes in the face of very poor results from some of Wall Street's bell weather stocks. Apple shares have been crushed from a peak of just over $700 to $590 today. Google shares are down over $100. Banking shares continue to languish and the S&P 500 is down 5% over the last two months. This economy needs jobs to maintain its recovery. Wall Street knows it and this is why the markets are turning over. So how do we get that going?

Well ask either of the presidential candidates and they are going to create millions of jobs overnight. We all know that is not going to happen, but I did stumble across one very interesting idea that may have a very good result. What if, instead of paying people unemployment benefits for 99 months we poured that money into removal of the minimum wage? A radical idea to say the least but let me clarify. If there was no minimum wage I know a number of businesses that would hire workers right away. Sure they would only pay them $5 an hour but that is far better than sitting at home wasting away. Once you are back at work the juices start to flow and suddenly you are able to find better opportunities.

Now here is the best part. The government would subsidize the difference between minimum wages and what the company pays the employee. So for example if the worker is paid $5 an hour but the minimum wage is $8 then the government would top up the workers pay at the end of each month. This three dollar difference would be far less costly and far more efficient in getting people back to work than our current program. Once a target of full employment is reached, there would be a slow re-introduction of the minimum wage, there would be a slow transfer of the burden back to the companies reducing the government's involvement. The idea is that at that time the economy would be at full employment so the demand for workers would bring the hourly rate up anyway and this would have the result of slowly reducing the government's burden as things improve. Furthermore a lot of the burden would be offset by the receipt of more tax revenues.

To me this idea has a lot of merit and is far superior to the money printing philosophy that we have in place right now. This philosophy has resulted in an economy that is still stagnant. Furthermore as I have repeatedly mentioned in this blog that the old ideas of pumping money blindly into a black hole are not targeted and are not producing the results that are needed but are creating a fiscal problem of the magnitude never before known.

The second piece of the puzzle is keeping interest rates low. This is key to the continued recovery in housing. A spike in interest rates would cripple the housing recovery which in turn would derail any form of moderate economic recovery. For now it seems that the continued transfer of toxic debt from banks to the Federal Reserve is containing interest rates but rates need to remain low for an extended time without printing money.

The first thing to do is to ensure as best as possible that banks are not involved in risky investments. In an article in Bloomberg it was mentioned that Dodd-Frank has done nothing to curtail banks enthusiasm for taking on risk. Furthermore as we have seen in crisis after crisis not only do bankers not fully understand risk but their greed gets the better of them and they need to be reigned in to abide by strict parameters. Let the hedge funds and alternative investment fund managers handle the risky stuff, banks need to be the backbone of the economy and the only way to do this is to limit the risk by increasing their reserve requirements. This is very simple to do but at present very risky as banks are already struggling to maintain current requirements while they unload their toxic debt. Increasing this now would cripple banks and put a big stake into the heart of their ability to lend. That said it should be ratcheted up over time to ensure that banks are not as vulnerable to systemic shocks as they were.

By strengthening the banking system with increased reserves and by increasing the base of employed workers I would argue that the economy would strengthen attracting foreign investors. This would keep interest rates low for an extended period. The only reason that interest rates would rise in this scenario is if magically Europe fixed its problems and there was reduced demand for perceived risk free investments. At this point interest rates would have to rise to attract investment. Outside of that unless inflation spikes interest rates should remain low, maybe not at the low levels they are right now but certainly not at massively elevated levels that people fear. A strong US economy would produce the desired result particularly while Europe struggles.

All of these ideas are relatively simple to implement but like any idea it would take time to produce the expected results however I believe those results would be achieved far quicker and far more cheaply than our current strategy. In the meantime we will have to deal with the approaching fiscal cliff and a globe that continues to be mired in uncertainty. Worse still we have an economy that does not have a repaired financial system and an economy that appears to be on the verge of a recession. Weak earnings, recession in Europe and problems in the United States are no reason to stay invested in an over inflated stock market.

Friday, October 26, 2012

How Will The Fiscal Cliff Get Resolved?

"I am quite concerned about Fiscal Cliff." - Alan Greenspan

"I am a firm believer in the people. If given the truth, they can be depended upon to meet any national crisis. The great point is to bring them the real facts." - Abraham Lincoln

"Any idiot can face a crisis - it's day to day living that wears you out." - Anton Chekhov